US Dollar Index struggles for direction around 92.00

- DXY alternates gains with losses around 92.00 on Tuesday.

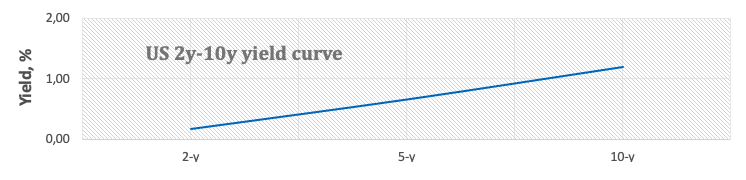

- US 10-year yields rebound from Monday’s lows near 1.15%.

- Factory Orders, FOMC’s Clarida, API report next on tap.

The dollar looks for direction in the. 92.00 neighbourhood when tracked by the US Dollar Index (DXY) on turnaround Tuesday.

US Dollar Index focuses on data

The index adds losses to the negative start of the week, although it manages well to keep business around the key 92.00 zone for the time being.

Recent weakness in the dollar comes amidst another knee-jerk in yields of the US 10-year note to as low as the 1.12% on Monday, where some initial contention seems to have turned up. Furthermore, the 2y-10y yield curve flattened on Monday by around 2 bps (from Friday).

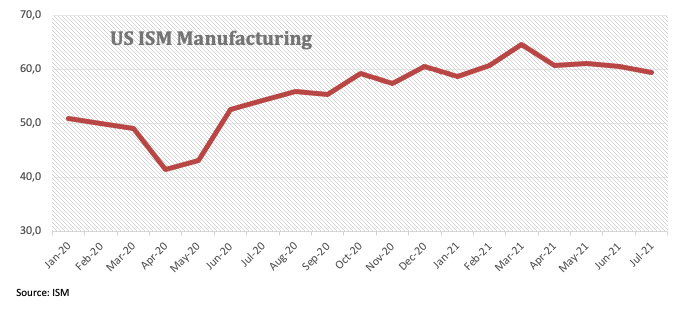

In addition, the lower-than-expected reading from the key ISM Manufacturing in July (released on Monday) collaborated with the bearish note surrounding the buck.

In the US data space, June’s Factory Orders will be in the limelight seconded by the IBD/TIPP Economic Optimism Index and the weekly report on US crude oil inventories by the API. Additionally, FOMC’s R.Clarida (permanent voter, dovish) is also due to speak.

What to look for around USD

DXY managed to put some distance from recent lows near 91.80, although still finds it difficult to gather serious upside traction above 92.00. The dollar remains under pressure after the Committee talked down the probability of QE tapering in the near term despite the upbeat, albeit so far insufficient, progress of the US economy. A clearer direction in the price action around the buck is now expected to emerge after the post-FOMC dust settles. In the meantime, bouts of risk aversion in response to coronavirus concerns, the solid pace of the economic recovery, high inflation and prospects of earlier-than-expected QE tapering/rate hikes should remain key factors supporting the dollar.

Key events in the US this week: Factory Orders (Tuesday) – ISM Non-Manufacturing, ADP report, MBA Mortgage Applications (Wednesday) – Initial Claims, Balance of Trade (Thursday) – Nonfarm Payrolls, Unemployment Rate (Friday).

Eminent issues on the back boiler: Biden’s multi-billion plan to support infrastructure and families. US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Debt ceiling debate. Potential hint at QE tapering at the Jackson Hole Symposium.

US Dollar Index relevant levels

Now, the index is losing 0.07% at 92.00 and faces the next support at 91.78 (monthly low Jul.30) followed by 91.51 (weekly low Jun.23) and then 91.33 (200-day SMA). On the upside, a break above 92.50 (20-day SMA) would open the door to 93.19 (monthly high Jul.21) and finally 93.43 (2021 high Mar.21).